“Money is like gasoline during a road trip. You don’t want to run out of gas on your trip, but you’re not doing a tour of gas stations. You have to pay attention to money, but it shouldn’t be about the money.” –Tim O’Reilly

Back in May I created a Kiva account, and funded it with $100. At the time I was feeling especially fortunate, and wanted to give something back.

Kiva is this really amazing non-profit organization that makes it possible for anyone to make microloans to people in developing countries. The best part is that I get to choose who my $100 goes to, in as small as $25 increments. So I chose four different applicants, two in Cambodia, one in Tanzania, and one in Vietnam. I didn’t realize it at the time, but all four were women. (In retrospect I consider this just retribution for all the unspeakable violence that has been, and continues to be, perpetrated against women around the world.)

One woman needed a loan to purchase a cow to reduce farming costs. Another needed a loan to buy a motorbike to commute to work more easily. And two others needed loans to further expand their poultry businesses. I didn’t fund their requests in full, but I didn’t need to. Many other Kiva members contributed a portion of the loans. You can check out all the details on my lender page: who I’ve lent to, who else has lent to them, the status of repayment, etc. It’s really quite engrossing.

With the money that’s been paid back so far, including one loan in full, I was able to lend $25 each to two women in Peru to purchase animals. Which means I’ve been able to make $150 worth of loans, even though I’d only “invested” $100. Put another way: my $100 has done $150 worth of good in the world. This makes me really happy.

One of the things I’ve heard people say about Kiva is that it’s addictive. It’s true, I didn’t want to stop at the two Peruvian women. So I decided to add another $75 to my account so I could lend to three more people, an aspiring restaurateur in Peru who buys and sells scrap iron, another Peruvian woman’s poultry business, and a couple in Cambodia who want to buy a cow for breeding.

What with all the mortgage crisis and bank failure drama in the news lately, I started to get the buy-a-home-of-my-own feelings again. As I’ve told Stephanie, all I really want to do is rip out the kitchen and install an Instant Kitchen. (Home Depot summer camp for adults anyone?)

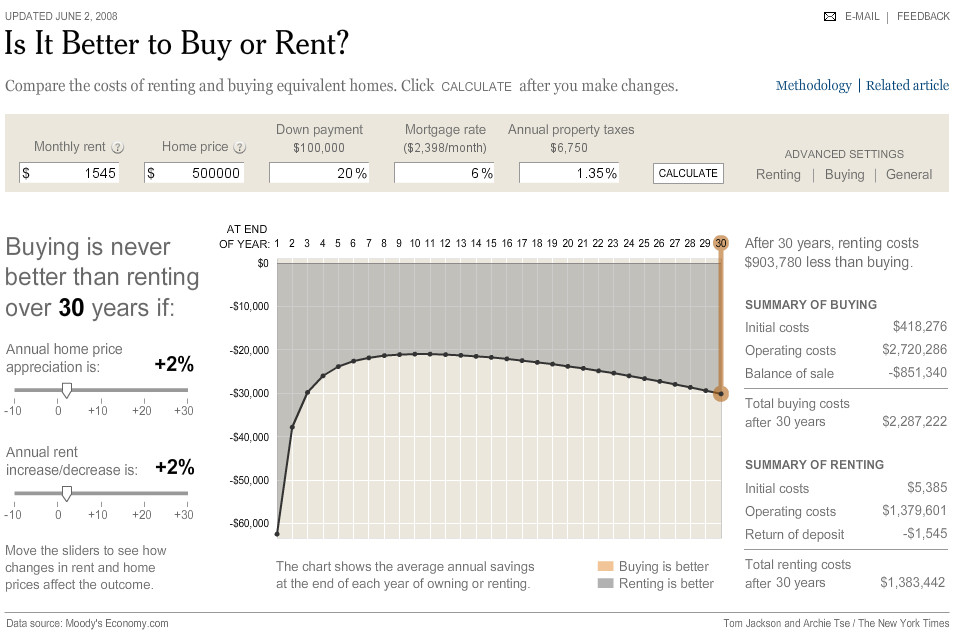

In order to get my head on straight I went back to the NY Times’ Is It Better to Buy or Rent? calculator. I like how it said (and continues to say) so unequivocally: Buying is never better than renting—assuming your rent is around $1500 and you’re looking at one bedroom condos in San Francisco, which start at $500k.

I mean maybe you could find something in the $400s, but it turns out that doesn’t help the picture much. Nor would it if our rent shot up to $2000—which our landlord let on is what they’re now renting the apartment above us for (two years in the city and rents have gone up $500…). No, owning doesn’t start to break even with renting until housing drops below 250k, something that will almost certainly never happen in San Francisco.

Which brings me back to where I started. Why buy?

Update: Perhaps this buy-a-home-of-my-own feeling is a cyclic thing. This post is a somewhat subconscious followup to one I wrote exactly a year ago: Thinking ahead (about real estate)

I know, I know you’re not supposed to check on your long term investments, but where’s the fun in that? I started investing money in the stock market (outside of my Roth IRA) last October, primarily in an index fund that tracks the S&P 500, but also in a bond market index, and as of May, an international large cap index. Since last October the market has only descended, almost 17% so far, which makes the numbers in my brokerage account all red and unhappy.

Thanks to bimonthly dollar-cost averaging, I haven’t lost that much. Overall I’m “only” down about 5% which is unsettling when compared to the 2.01% I’m getting on my checking account. But at the same time I’ll admit it’s pretty cool, because it’s like my money takes on a life of its own. It’s much more dynamic than money just percolating in a savings account. Even though my investments are a small drop in the global pool of money, it’s neat to think they’re indirectly making it possible for businesses here and abroad to do their thing.

Last week on the ride home I noticed a marked reduction in power accelerating from a stop along Lombard. At each light, I felt the same thing, almost as if the throttle’s connection to the engine had become a rubber band. I could get up to speed, but it took a long time getting there. I thought I also heard some rattling, but with a helmet on, it was hard to tell if it was coming from the scooter or from another car. The next morning I had Stephanie take it for a ride around the block, and she confirmed that something was really wrong.

Conveniently the San Francisco Vespa dealership is only a few blocks away, but somewhat annoyingly, there’s a month lead time for appointments, and this just couldn’t wait. It was even more pressing when I realized I had just 4 days left on my year warranty before it expired. I called to see if they could squeeze me in, and their response was pretty much: “Maybe.” This burned me a little, but I dropped it off anyway, and crossed my fingers.

Third Service, new rear tire

Well it turns out they did fit me in, discovered a busted “clutch pulley” and were able to replace it under warranty (saving me $260). Since I was almost at 4000 miles, I decided to have them perform my 3rd service and replace a bald rear tire. Total cost: $568.03. At which point most car owners would be cringing. I suppose owning a Vespa saves me money in a number of ways, but maintenance, at least through a “certified dealership” is not one of them. Since I’m coming up on a year of Vespa ownership, I though it might be illuminating to detail my maintenance costs thus far, for any prospective LX150 buyers out there.

First service, brush touch up

The dealership charges $150 for the first service. If I had bought the scooter from them directly instead of via Craigslist, they would have reduced the price of labor by 40%. That said, when I make an appointment online, they knock 10% off the price, bringing the first service down to $135. Before I brought it in, my scooter had been knocked over, miraculously only getting three little scratches on the right cowl. When I pointed it out, they offered to touch it up, I figured it wouldn’t cost that much. They charged $150! Basically painting over three scratches with the equivalent of black nail polish. That burned me a lot. I also learned a lesson in vanity, as my scooter was tipped over again not long after, completely negating their overpriced brush touch up. So total cost of the first service: $286.60.

New battery

At just over 2,000 miles, in time for my 2nd service, the scooter was starting to sound like it didn’t have enough juice to start the engine. On several separate occasions I actually had to have it jumped! I wasn’t totally surprised, because the same thing happened to Stephanie at exactly the same mileage (perhaps it had something to do with our scooters being tipped). In any case, I made an appointment for the service, but again, they didn’t have any available openings for a month and a half. So I went down to First Kick Scooters, and they installed a larger, sealed battery, originally intended for the ET4 model. Apparently the factory LX batteries are known to lose their juice, which kind of burns me (thanks for nothing Vespa). The new battery cost $112.72.

Second service

When I finally made it to my 2nd service appointment, I was at 2,915 miles. The second service usually costs $250, but with the 10% wait-a-month-and-a-half discount, the total was “only” $226.50. Apparently for that they changed my oil and replaced the filter, plus all “necessary adjustments and checks”. Talk about a pricey oil change. Here’s the rub: the Vespa warranty is void if I have the scooter serviced at a non-certified shop. So essentially I’m being held hostage by Vespa.

Total

In total, with the 3rd service I already mentioned above, I’ve spent $1,193.85 on maintenance over the last year, of which only the $150 brush touch up could be considered unnecessary, though at the same time I lucked out that the $260 clutch pulley replacement happened within 4 days of my warranty expiring. So for a vehicle that only cost me $4300, I’ve already spent 27% of purchase price on maintenance. Ouch. I don’t know if I’m paying a San Francisco labor premium or what, but I’m not sure I’m going back to the Vespa dealership now that my warranty has expired.

Gear, insurance, parking

And of course that total does not include the cost of riding jackets, rain gear, helmets, and gloves which I’ve probably spent about $500 on. Or $500 a year on insurance. Or $60 a year for city street parking plus the inevitable parking tickets (I’ve probably gotten 3-4 so far at $40 a pop).

All that said, I love my Vespa. I wish it looked better, but it’s a tool, not a museum piece. It allows me to get to work on my schedule, and park in the city where ever I want.

I’ve recently discovered something about myself: I find the rise and fall of the stock market endlessly fascinating. Actually that’s a bit of hyperbole. I just haven’t found an end to my fascination.

As I’ve blogged previously, I’ve invested my retirement and long term savings into some broad mutual (SWERX) and index funds (SWPIX and SWLBX). In both cases, I’ve subscribed to the dollar cost averaging strategy of investing—invest a fixed dollar amount every quarter/month/week ($416.66 every month in the case of my IRA). When the market is high, I automatically buy less shares, when the market is low, I buy more.

For the geeks, think: investing as a cron job.

I should add that doing all this doesn’t take lots of money, or any special knowledge, beyond a little research. It just takes a commitment to yourself to save a little bit of money each month. All I did was open a Roth IRA account at Schwab (which could just as well have been with Fidelity, Ameritrade, my bank, etc.), initiated an automatic monthly transfer from my checking account (which was Wells Fargo at the time) to my Schwab account, and then followed that up with an automatic investment into a mutual fund.

Anyway, towards the end of last year/beginning of this, I’ve watched my retirement account lose 9% of its value, which is pretty shocking in terms of dollar amount (I might be in for a real shock when the market reopens tomorrow)—but who cares, I can’t touch the money until I’m 59.5.

The good news is that as the market plummets, I’ll just end up buying more shares at lower prices each month, which should work out in the long term when the market eventually rebounds (hopefully sometime between now and the year 2040).