“Money is like gasoline during a road trip. You don’t want to run out of gas on your trip, but you’re not doing a tour of gas stations. You have to pay attention to money, but it shouldn’t be about the money.” –Tim O’Reilly

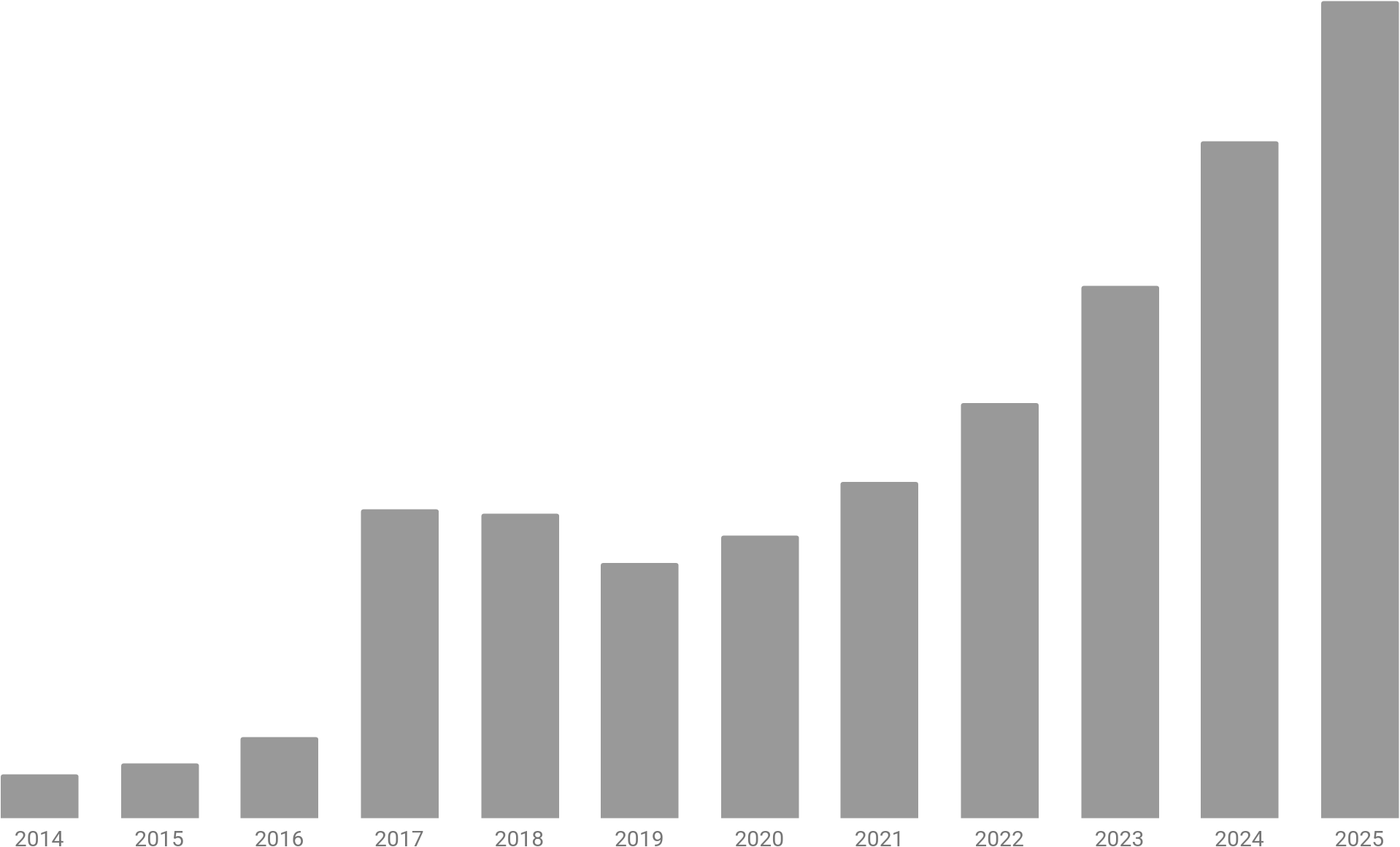

At the end of every month I record the balance of our retirement and brokerage accounts in a spreadsheet. At some point, after having maintained this practice for several years, I created a separate spreadsheet with the combined total across our accounts taken from the end of each year. I use this data to generate a simple graph that shows the change in value of our investments over time.

With one notable exception, our savings strategy in 2024 was identical to the year prior: max out our pre-tax retirement plans at work, i.e., Stephanie’s 403(b) and my Individual 401(k), and max out our traditional IRAs—if allowable. And allowable it was, because our modified AGI was below the “phase-out threshold for MFJs covered by retirement plans at work” ($123,000 in 2024), and our AGI was below that threshold precisely because we had maxed out our pre-tax retirement plans at work. Put simply, our 401(k) plus 403(b) contributions reduced our taxable income to the point where we could also make traditional IRA contributions, which further reduced our taxable income. All together these retirement contributions saved over $13,000 in state and federal income taxes.

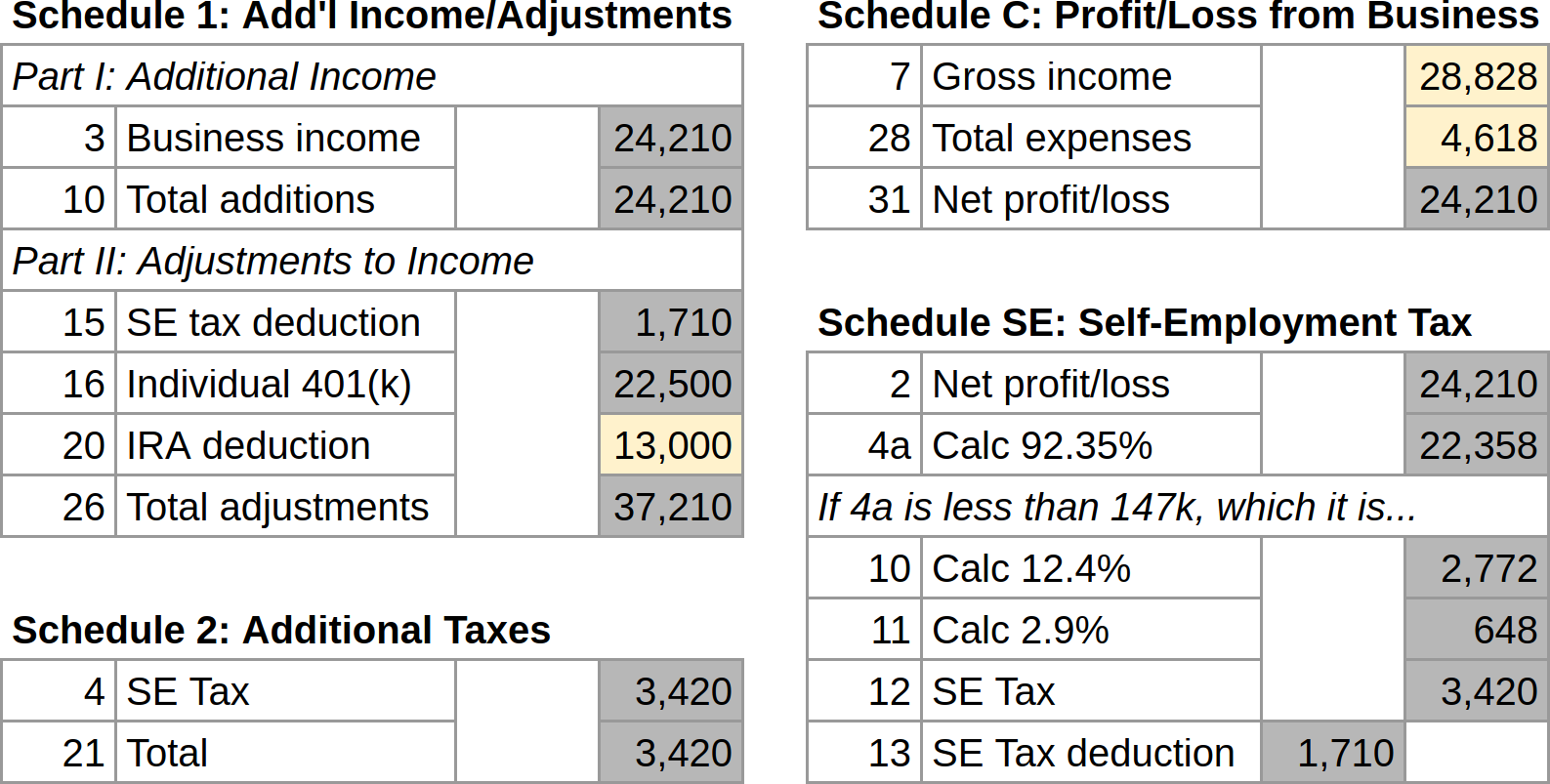

Though I’m still internalizing the fact that I was self-employed last year, the IRS needs little convincing. With net earnings from self-employment over $400, they consider me very much self-employed, and those earnings need to be reported. To be honest, this is something I’ve been chomping at the bit to do for some time, because it unlocks a brand new savings achievement: the Individual 401(k)! Also known as a Solo 401(k), it will allow me to contribute (read: defer) far more of my self-employment income than I could with just an IRA, plus I’ll gain the potential to make “profit-sharing” contributions as the plan’s employer.

To figure out how much I’d be able to contribute, I needed to do a dry run of our taxes. So back in November, I dusted off the spreadsheet I built to simulate Form 1040 and added the following to account for my self-employment income: Schedule 1 (Additional Income and Adjustments to Income), Schedule 2 (Additional Taxes), Schedule C (Profit or Loss From Business), and Schedule SE (Self-Employment Tax). Though that may sound like a lot, I only needed to input 4 values (highlighted in yellow) across those 4 schedules. The values in gray are simply references to other cells or basic calculations.

Screenshot of my spreadsheet simulating the IRS Form 1040 Schedules 1, 2, C, and SE for 2023

I like to reflect on the financial decisions I’ve made over the past year because trying to explain them, in writing, ultimately forces me to better understand the machinery involved, and often suggests additional actions I might consider taking, now or in the future.

“I’m sure you know the quote ‘Writing is nature’s way of letting you know how sloppy your thinking is’, and knowing how sloppy your thinking is allows you to sharpen it, test your arguments, and test different explanations. I find, more often than not, that I understand something much less well when I sit down to write about it than when I’m thinking about it in the shower. In fact, I find that I change my own mind on things a lot when I try to write them down. It really is a powerful tool for finding clarity in your own mind.” —Marc Brooker in Writing Is Magic

This was the “back-of-the-envelope” analysis (to which I’d previously alluded) that convinced us to buy a house in Fresno for the duration of Stephanie’s 3-year doctoral program.