Learning how to save, fifteen years later

There was a time when I couldn’t wait to start drafting these annual reports. And then, 3 years ago, I stopped working. Without income to save, I thought, what did I have to say about saving? Only recently have I begun to appreciate how that sense of the word, what financial planners call “accumulation”, obscures another sense: “preservation”. And maybe I have learned a thing or two about the ebb and flow of preservation.

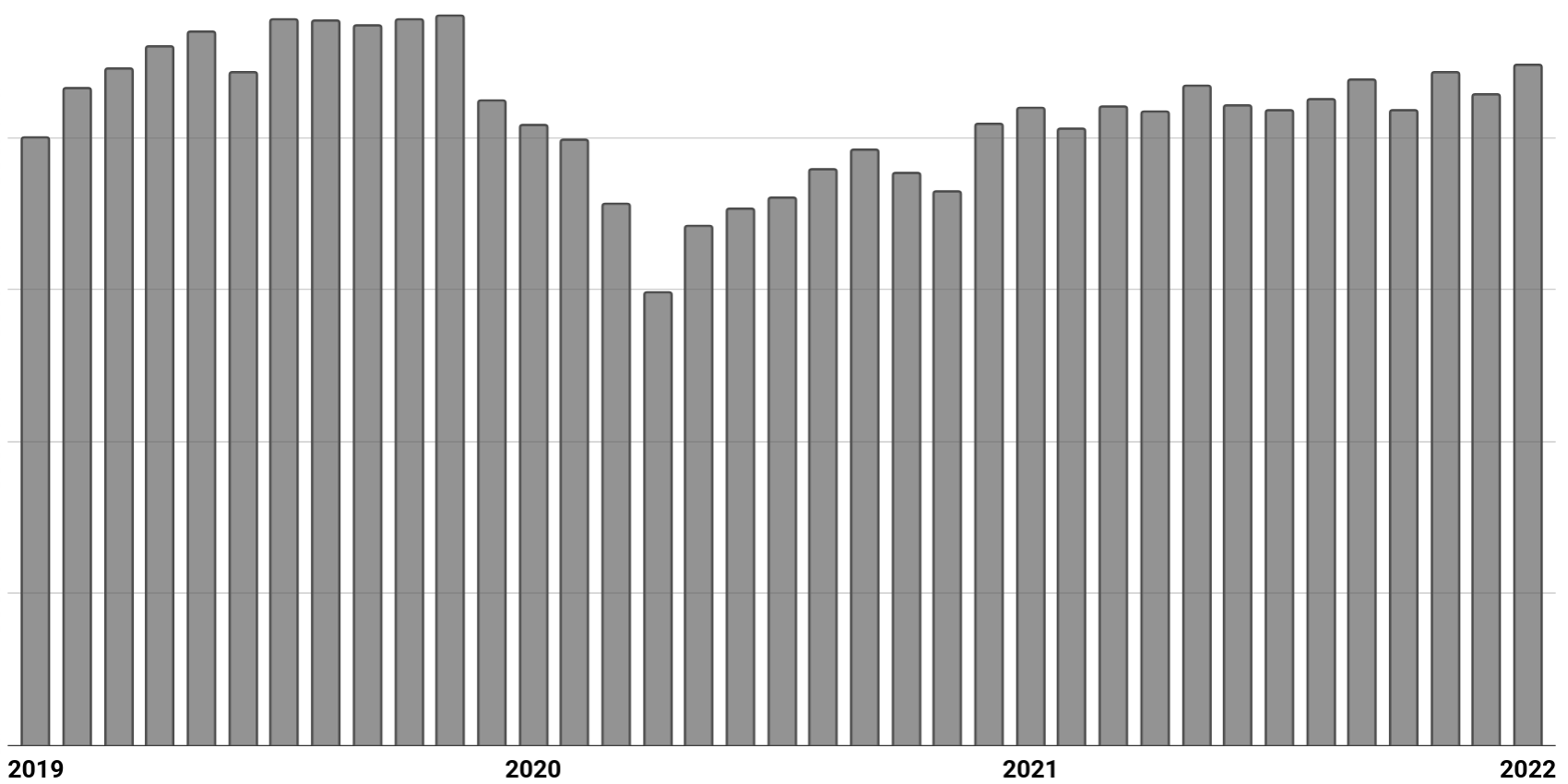

The full extent of our savings (spread across a handful of taxable and tax-advantaged accounts) are still invested in a single S&P 500 index fund. No change there. But without the regular influx of cash from a paycheck, every few months I sell shares from one of our taxable accounts to cover our expenses. Think of it as dollar-cost-averaging on the sell-side. What floors me is how well our taxable accounts have maintained their value over the last 3 years—even in the face of a protracted pandemic.

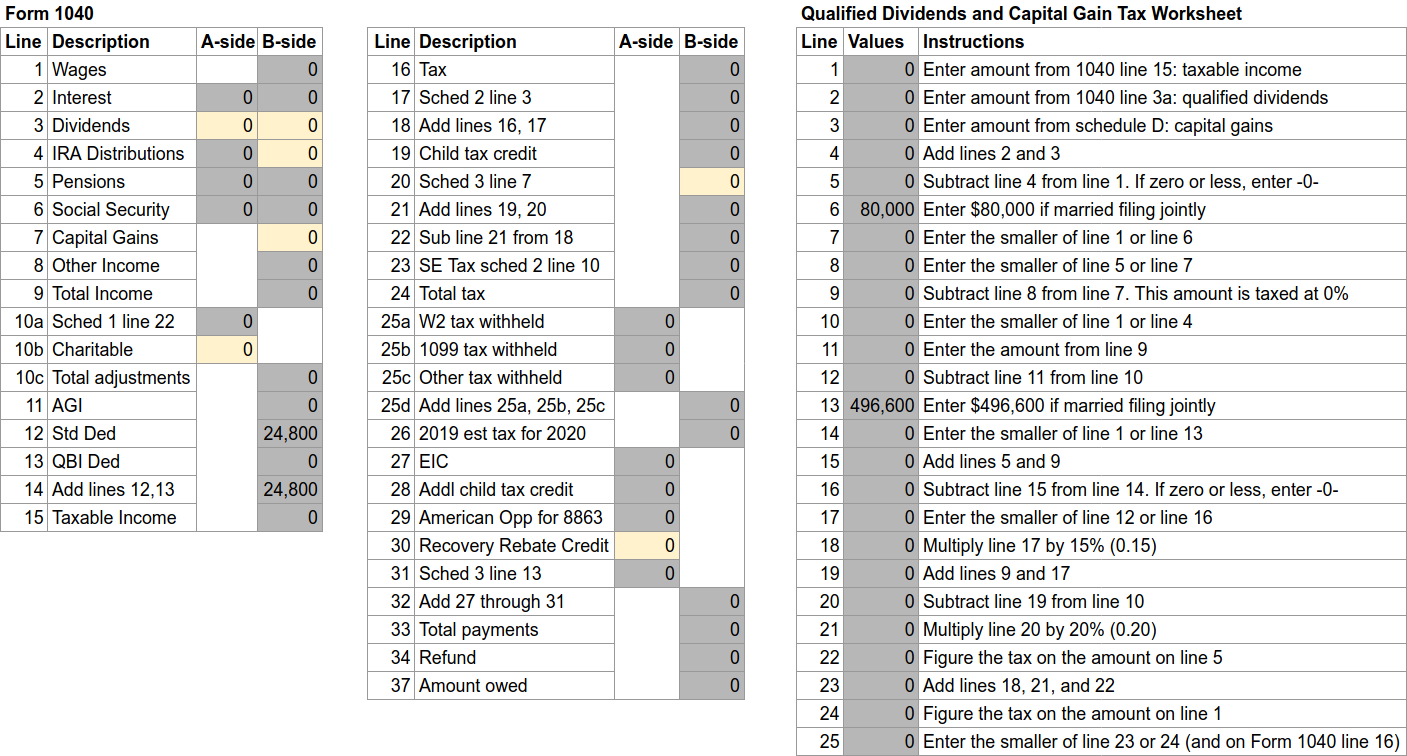

Though I stopped working at the end of 2018, I did earn some income the following January (in the form of a bonus). This meant that 2020 was really my first year without any earned income, and thus my first opportunity to initiate a Roth IRA conversion without incurring any federal taxes—a move I’ve been keen to make since wrapping my head around “how taxes work” in 2016. The key concept is that the first $24,800 of income was taxed at 0% in 2020 (also known as the “standard deduction” for MFJs). Since I didn’t have any earned income, in essence I could “create income”—at least $24,800, in theory—by transferring funds to my post-tax Roth IRA from my pretax traditional IRA (into which I had previously rolled over the balance of my pretax 401(k)). As a side note: we did have some unearned income in the form of qualified dividends and long-term capital gains, of which the first $80k was not taxed, and we were waaay below that threshold. I wrote “in theory” above because I was pretty sure I could actually convert quite a bit more, thanks to Stephanie’s eligibility for a $2,000 Lifetime Learning Credit and the remainder of our Recovery Rebate Credit. But I wasn’t sure how much more. This compelled me to do something a little crazy that I’d never attempted before: I created a spreadsheet to simulate IRS Form 1040 and the “Qualified Dividends and Capital Gain Tax Worksheet”. 🔥

By adjusting the values in a handful of cells (those highlighted yellow above, primarily Line 4b for Taxable IRA Distributions), I was able to dial in precisely how much I could convert without owing any tax. When I eventually got around to filing our taxes, I discovered that though my spreadsheet calculations were spot on, I had under-estimated our Recovery Rebate Credit—turns out I could have converted even more. Instead we got a healthy refund that offset the California state taxes we owed (as California’s standard deduction in 2020 was only $9,202, and dividends and capital gains are taxed as ordinary income). Without any earned income in 2021, I updated the spreadsheet and again used it to calculate how much to convert. This may be my last opportunity to employ this strategy, at least for a while, as Stephanie plans to seek a job after she graduates in May, in which case her earned income in 2022 will likely fill up our standard deduction bucket.