Learning how to save, seventeen years later

Though I’m still internalizing the fact that I was self-employed last year, the IRS needs little convincing. With net earnings from self-employment over $400, they consider me very much self-employed, and those earnings need to be reported. To be honest, this is something I’ve been chomping at the bit to do for some time, because it unlocks a brand new savings achievement: the Individual 401(k)! Also known as a Solo 401(k), it will allow me to contribute (read: defer) far more of my self-employment income than I could with just an IRA, plus I’ll gain the potential to make “profit-sharing” contributions as the plan’s employer.

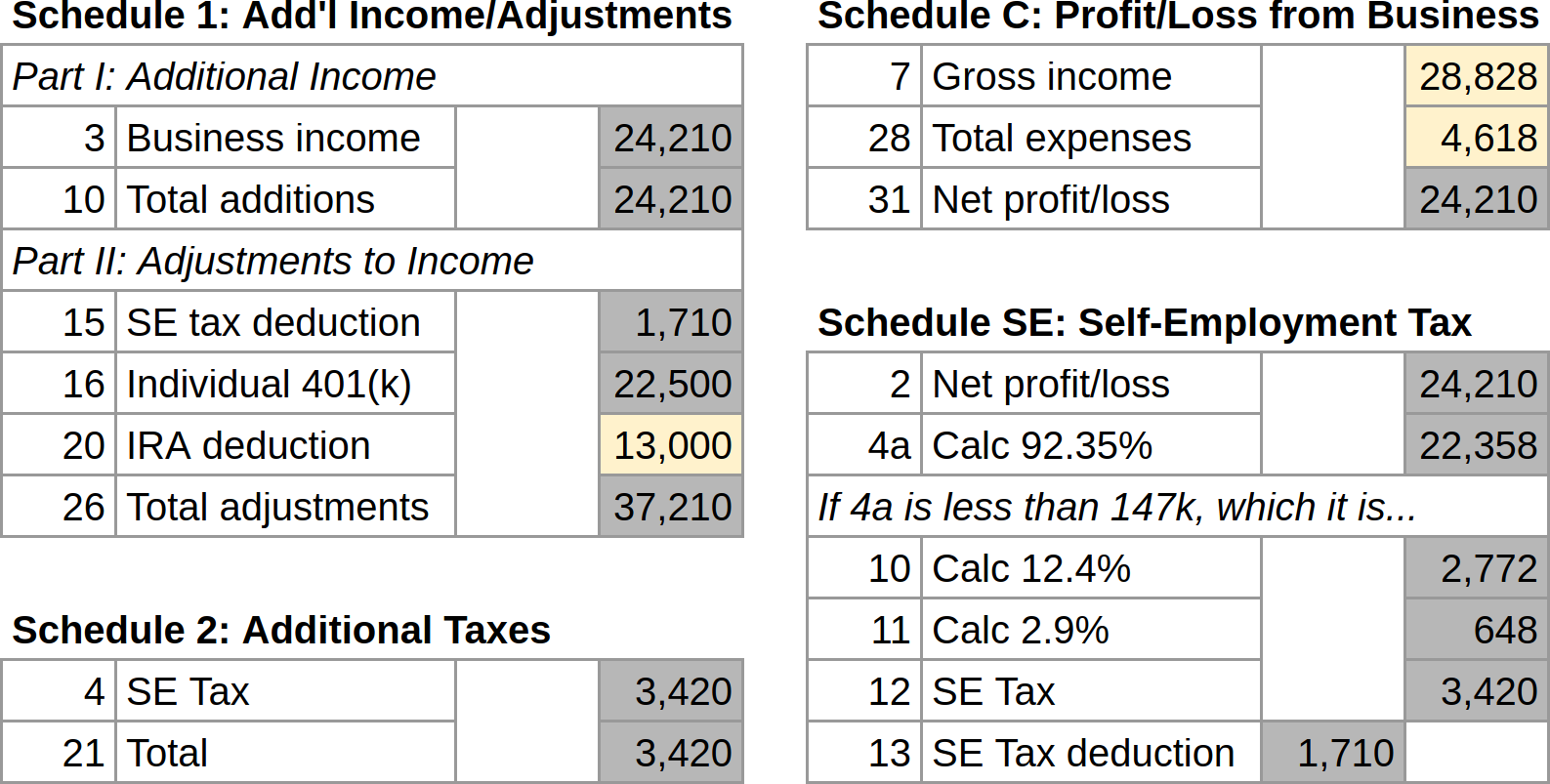

To figure out how much I’d be able to contribute, I needed to do a dry run of our taxes. So back in November, I dusted off the spreadsheet I built to simulate Form 1040 and added the following to account for my self-employment income: Schedule 1 (Additional Income and Adjustments to Income), Schedule 2 (Additional Taxes), Schedule C (Profit or Loss From Business), and Schedule SE (Self-Employment Tax). Though that may sound like a lot, I only needed to input 4 values (highlighted in yellow) across those 4 schedules. The values in gray are simply references to other cells or basic calculations.

As an aside: the beauty of building my own tool is that I only have to implement the features that are relevant to my particular circumstances (and as such, YMMV). I find my minimalist spreadsheet above so much easier to parse than the equivalent 8 pages of IRS forms spread out across the kitchen table—not to mention the fact that the spreadsheet calculations automatically update whenever I make changes, whether actual or hypothetical. Some tools it can be hard to imagine having ever lived without; this has become one of those for me.

The first OMG of this effort was seeing the Self-Employment (or SE) Tax number climb steadily through the end of the year, until it landed on $3,420. Ouch. There’s a lot you can do to reduce your federal and state tax burden, but the SE Tax, which is composed of Social Security (aka OASDI) and Medicare, takes the first cut. And when you’re self-employed, that cut is an eye-watering 15.3% (update: actually the “cut” ends up being 14.12955%, because the 15.3% only applies to 92.35% of the net profit)—whereas someone who’s “employer-employed” only sees Social Security and Medicare take 6.2% and 1.45%, respectively, because their employer sneakily pays the other half of both on their behalf. Oddly enough, it was the 15.3% SE Tax value that I needed in order to calculate my maximum Individual 401(k) employee contribution, which turns out to be net profit minus one-half of the SE Tax (up to $22,500 in 2023). This is where things might seem a little spooky, because my net profit of $24,210, minus one-half of my SE Tax, or $1,710, just so happens to be $22,500! Suffice it to say, I was deliberate about which expenses I chose to deduct. I also got lucky, as I reached that net profit of $24,210 on December 28th, working my very last gig of the year.

The reality of these numbers might seem contradictory. How can someone who’s self-employed make a $22,500 contribution to their Individual 401(k), let alone eat and pay rent, if they only have $20,790 leftover after paying their SE Taxes? (That math, by the way, is: $24,210 – $3,420 = $20,790.) It goes without saying that you can only contribute to a retirement account what is financially feasible given your own circumstances, but it is also easy to forget that money is fungible, so once the contribution maximum is known, the funds to contribute could conceivably come from anywhere: the money sitting in a business checking account, last year’s profits squirreled away in a savings account, a gainfully employed spouse who’s pulling down a regular salary, etc. In my case they came from a combination of the surplus earnings I’d built up toward the end of the year, the annual dividends we earned in our brokerage accounts (which, for the first time ever, I chose not to have automatically reinvested—for exactly this purpose), plus a small sale of our S&P 500 index fund to make up the rest (the net effect of which was essentially money moving from one bucket to another).

And then there’s the Qualified Business Income (or QBI) deduction (on line 13 of Form 1040). For the last few years TurboTax would fill it in for me with some measly value of around $50 from the dividends generated by REITs in our S&P 500 index fund. But with self-employment income last year, I discovered that I could deduct 20% of my net profit as a QBI, which would reduce my taxable income by a further $4,842! Of course with only my income at play, that QBI deduction wouldn’t take effect, since my 401(k) contribution and the one-half SE Tax deduction will have already reduced my taxable income to $0 ($24,210 – $22,500 – $1,710 = $0), but since Stephanie and I file jointly, the QBI deduction ultimately ends up reducing her taxable income. Update: Alas, I was wrong. Turns out the QBI deduction is calculated off the net business income after qualified retirement contribution deductions, so for QBI purposes my net business income was $0, thus no QBI deduction for me. See How The New QBI Deduction-Reduction Ruins The Value Of Pre-Tax Retirement Plans For Small Business Owners for the grisly details.

Stephanie’s income, being neither too high nor too low—in no small part because she maxed out her 403(b)—allowed her to max out contributions to both of our traditional IRAs, even further reducing her taxable income. (Note: that was the 13,000 value highlighted yellow in Schedule 1 of my spreadsheet above.) This litany of deductions would have resulted in a pretty sweet refund (of the federal income tax her employer withheld), had it not been for my $3,420 SE Tax liability, which devoured any refund and then some. To head off a potential underpayment penalty, I made a one-time direct payment to the IRS, and then Stephanie updated her W-4 to withhold an additional amount per paycheck to cover my SE Tax liability going forward—yet another benefit of having a gainfully employed spouse. (The alternative would have been for me to make estimated quarterly tax payments.)

Before this year, I focused my tax simulation efforts entirely at the federal level and treated California as a back-of-the-envelope, hand-waving afterthought. But given my lack of prior experience with self-employment taxation, I was a little worried about getting dinged by California. For instance, 0.9% of Stephanie’s pay in 2023 went to something called the California State Disability Insurance program, or CA SDI. Would I have to pay that? Turns out no, disability insurance in California is optional if you’re self-employed, go figure. In any case, I went through the trouble of adding California’s Form 540 to my spreadsheet, and I was pleasantly surprised to discover that since I had fully deducted my self-employment income (again, in the form of my Individual 401(k) contribution and the SE Tax deduction), from California’s perspective, I had been a couch potato all year. And since California has nothing comparable to the federal SE Tax, the state had nothing to ding me with. Furthermore, our traditional IRA contributions helped to offset our dividends and long term capital gains (that California taxes as regular income), which, along with qualifying for the Renter’s Credit, means we should actually receive a healthy refund! Granted it won’t be enough to compensate for my SE Tax bill, but still, it’s not nothing.

2023 ended up being something of a watershed year for us. Stephanie earned her first full year of income since 2013, and I earned my first income since 2018. But that said, our spending and saving habits, informed by many years living off of a single income and then none at all, have remained fairly steady and relatively impervious to inflation (lifestyle or otherwise). As far as this coming year is concerned, I’m reminded of the pithy financial disclaimer: “Past performance is no guarantee of future results.” Maybe it’s because we’ve had 5 different addresses over the last 10 years, or maybe it’s the toll taken by the pandemic, climate change, multiple economic crises, et al., or maybe I’m just getting older (and possibly wiser?), but I’ve become less willing to entertain that anything in the future is guaranteed. I’m not sticking my head in the sand and refraining from making plans, but I do try to stay as flexible as possible and open to changing conditions on the ground. Which is to say, I have no idea what 2024 holds.