“Money is like gasoline during a road trip. You don’t want to run out of gas on your trip, but you’re not doing a tour of gas stations. You have to pay attention to money, but it shouldn’t be about the money.” –Tim O’Reilly

There was a time when I couldn’t wait to start drafting these annual reports. And then, 3 years ago, I stopped working. Without income to save, I thought, what did I have to say about saving? Only recently have I begun to appreciate how that sense of the word, what financial planners call “accumulation”, obscures another sense: “preservation”. And maybe I have learned a thing or two about the ebb and flow of preservation.

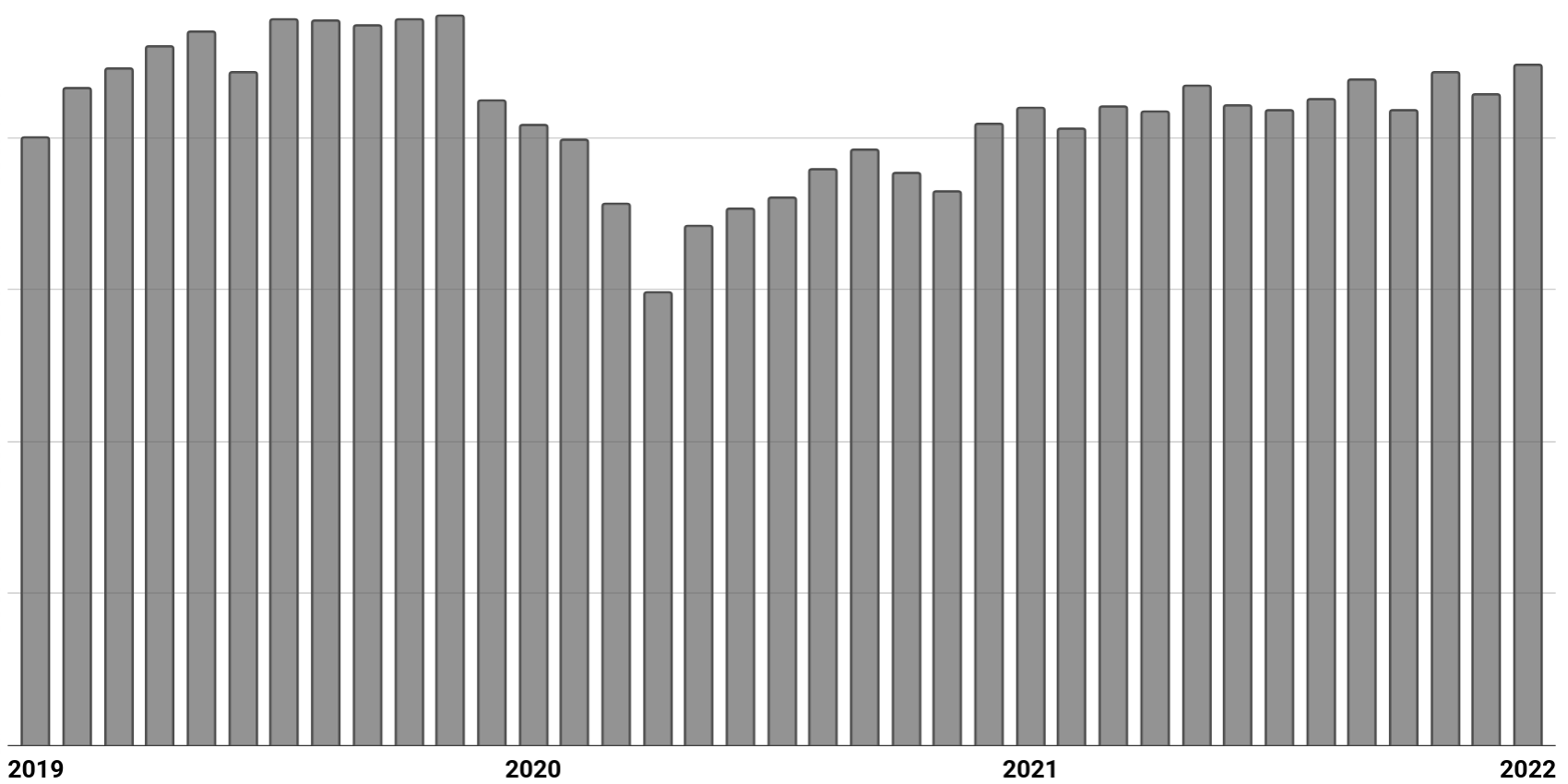

The full extent of our savings (spread across a handful of taxable and tax-advantaged accounts) are still invested in a single S&P 500 index fund. No change there. But without the regular influx of cash from a paycheck, every few months I sell shares from one of our taxable accounts to cover our expenses. Think of it as dollar-cost-averaging on the sell-side. What floors me is how well our taxable accounts have maintained their value over the last 3 years—even in the face of a protracted pandemic.

Monthly value of our taxable accounts from January 1, 2019 to January 1, 2022

Landscaping drew me in for a number of reasons, but I had completely forgotten about one until digging it up recently: on February 3, 2020, I got an estimate back from a landscaper that seemed so astronomically high, I decided I just had to start doing the work myself. I hired a tree service company to do what I couldn’t, and they showed up the very next day. You know how people say “Oh, you must be saving a ton of money doin’ that yourself”? My reaction is usually, “I dunno, I’m at Home Depot like every other day,” because it feels like I’m actually spending a ton, but at least I’m learning a ton, and I think I’m getting a better result in the end.

You’d think I’d have found time to write this while “snowbound in Tahoe”, but my priorities then were jigsaw puzzling, snowshoeing, and cooking good food from scratch, full stop. In truth, Stephanie did most of the jigsaw puzzle, because I had begun puzzling over something else: where to live once she had chosen Fresno State for grad school.

We’d already surveyed several apartment complexes, so we had a good sense of the quality and price points available. But still I found myself asking the question, what if we bought a place? How would 3 years of rent compare to the costs unique to buying a house (i.e. real estate agent commission, property tax, homeowner’s insurance, closing costs, etc.)?

My back-of-the-envelope and admittedly flawed analysis (“flawed” because I assumed both a flat stock market and a flat housing market; also I didn’t foresee the extent of the renovations we’d take on, nor can I predict the impact they’ll have on a future sale) suggested that we’d throw away more money renting over three years than buying, even without any price appreciation. So I started looking at listings, got in contact with an agent, and we found ourselves in contract on a house while still in Tahoe.

A short quiz: If you plan to eat hamburgers throughout your life and are not a cattle producer, should you wish for higher or lower prices for beef? Likewise, if you are going to buy a car from time to time but are not an auto manufacturer, should you prefer higher or lower car prices? These questions, of course, answer themselves.

But now for the final exam: If you expect to be a net saver during the next five years, should you hope for a higher or lower stock market during that period? Many investors get this one wrong. Even though they are going to be net buyers of stocks for many years to come, they are elated when stock prices rise and depressed when they fall. In effect, they rejoice because prices have risen for the “hamburgers” they will soon be buying. This reaction makes no sense. Only those who will be sellers of equities in the near future should be happy at seeing stocks rise. Prospective purchasers should much prefer sinking prices.

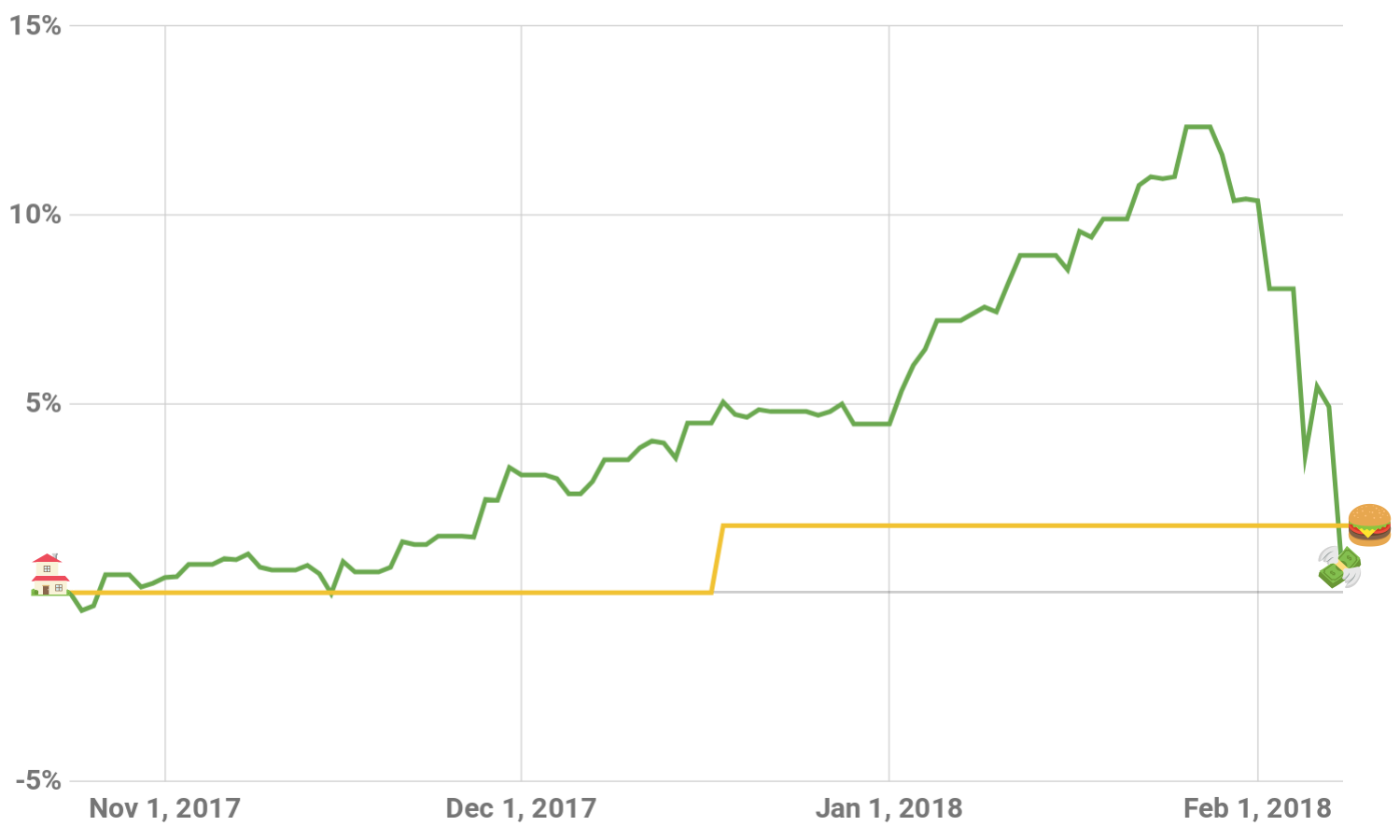

When we sold our condo last October, I invested 100% of the proceeds in Schwab’s S&P 500 index fund (SWPPX). It was pretty exhilarating to watch it climb in value practically every day, all the way through January 26th, at which point it had increased by 12.3% in only 3 short months. Since then, it’s been no less exhilarating to watch it drop precipitously in value, essentially retreating back from whence it came, in only 2 short weeks. This seemed like the perfect opportunity to contrast the volatility of value against the stability of ownership. Though the market has risen and fallen dramatically over the last 4 months, I still own the same number shares—in fact I actually own almost 2% more than I started with, because I reinvested the dividends and capital gains that were paid out in mid-December.

Percent Change of S&P 500 Index Fund Value vs. Shares

I’ve been writing these annual reports for 11 years, starting in 2006. But if you only looked at a graph of my investment contributions over the same time period, you might assume that I’ve only been really serious about saving during the last 4 years. And there might be some truth to that.

Investment contributions from income by account, 2006–2017

The trigger for the change, counterintuitive as it may seem, was Stephanie quitting her job in 2014. My reaction to this voluntary reduction of our collective income, coupled with an indeterminate timeline (at first we thought 8 months—but if Stephanie completes her graduate program as planned, it will end up being 8 years!), was to impose a savings-based austerity program on my income. I increased my 401(k) contributions, funded both of our Roth IRAs (through “the backdoor”), and invested “The Rest” (essentially an arbitrary round number that I pulled out of a hat) in my brokerage account—starting in 2014 and continuing every year since.