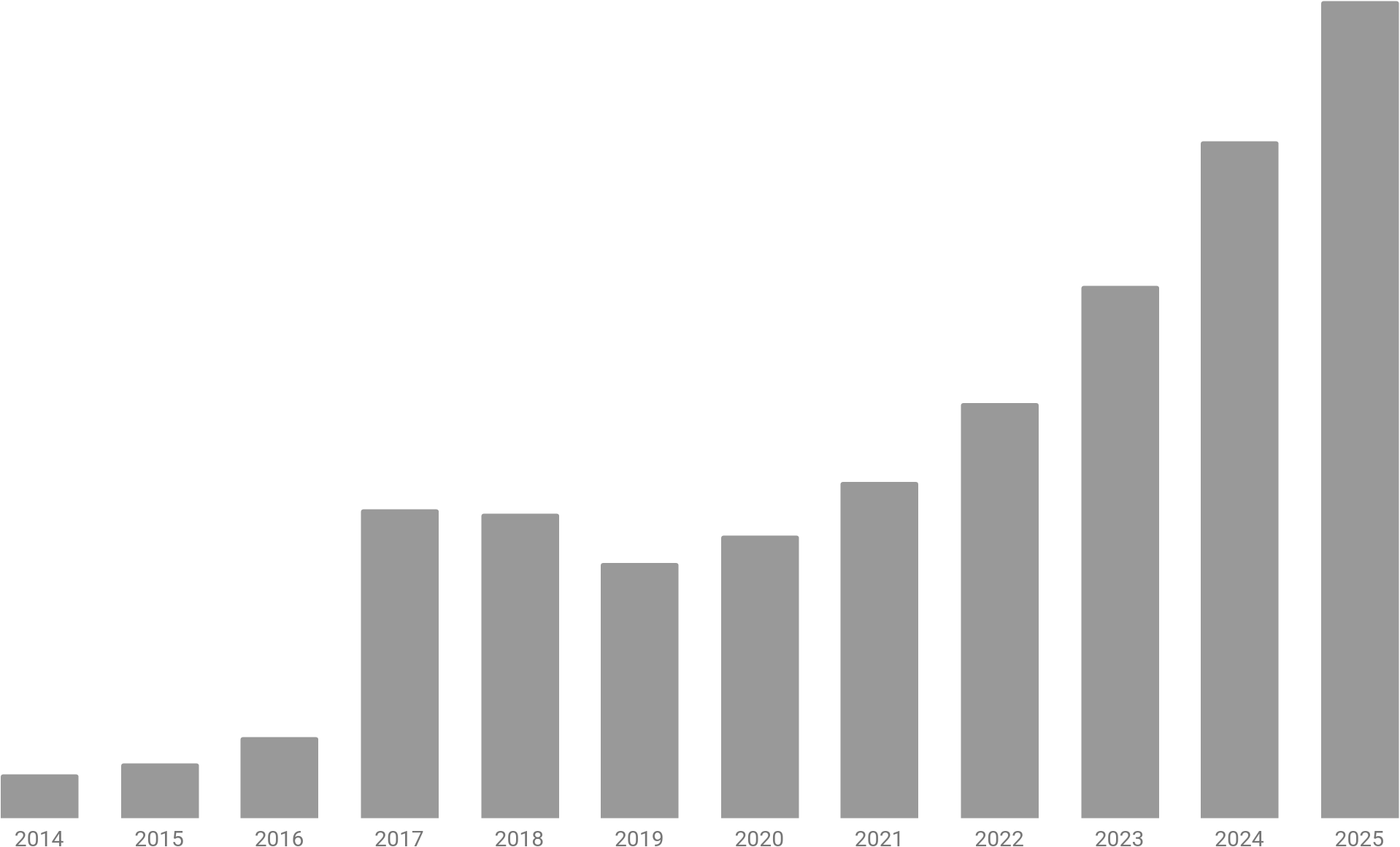

At the end of every month I record the balance of our retirement and brokerage accounts in a spreadsheet. At some point, after having maintained this practice for several years, I created a separate spreadsheet with just the combined total across our accounts taken from the end of each year. I use this data to generate a simple graph that shows the change in value of our investments over time.

Heartened to learn these exist, disheartened that they must.

“Since the election, the Immigrant Legal Resource Center, which is headquartered in San Francisco, has received orders for about nine million [red] cards, more than in the previous 17 years combined.” —The New York Times

With one notable exception, our savings strategy in 2024 was identical to the year prior: max out our pre-tax retirement plans at work, i.e., Stephanie’s 403(b) and my Individual 401(k), and max out our traditional IRAs—if allowable. And allowable it was, because our modified AGI was below the “phase-out threshold for MFJs covered by retirement plans at work” ($123,000 in 2024), and our AGI was below that threshold precisely because we had maxed out our pre-tax retirement plans at work. Put simply, our 401(k) plus 403(b) contributions reduced our taxable income to the point where we could also make traditional IRA contributions, which further reduced our taxable income. All together these retirement contributions saved over $13,000 in state and federal income taxes.

I speculated at the end of 2023 that the initial slowness in my schedule may have had less to do with the inclement weather and more with “my lack of any regular clients. With the latter now in place, it’ll be interesting to see how the early part of 2024 plays out.” Well, the year started out both rainy and slow, but when the clouds parted and people emerged from their post-holiday hibernation, my theory proved prescient. Of the ten clients with whom I worked in January and February, only three were new.

Not the first time a client lent me their truck to take a load to the dump