This was the “back-of-the-envelope” analysis (to which I’d previously alluded) that convinced us to buy a house in Fresno for the duration of Stephanie’s 3-year doctoral program.

Apparently I wasn’t alone. For reasons known only to The Algorithm, “Timber Frame vs Conventional Stick Frame” blew up (to the point that a follow-up was uploaded in March to assuage the rabble). I had resisted watching it, I think because that ubiquitous thumbnail looked so academic. At the time I was more into watching people actually build homes, most notably Woodness Goodness’s Cabin Build, Crafted Workshop’s (Not So Tiny) Tiny House Build, and Essential Craftsman’s Spec House Series. It wasn’t until November, after I’d finished landscaping the front yard, supporting my Dad on the CDT, and digging another dry well, that I finally took the bait. Certainly my renovation projects over the last 3 years had primed me, but it’s astounding in retrospect that it only took 6 minutes to go from knowing nothing about timber frames, to knowing with absolute clarity that I would—one day—build a timber frame home. And I don’t mean “build” as in “have someone build”, I mean “build with my own two hands”.

“Have you ever built a house with your own hands, out of the materials that Nature left lying around? Everyone should have that experience once. It is the most satisfying experience I know. We have been as fascinated as children who build forts or snowhouses, and it has made us the tightest little society in all the West.” —Susan Burling Ward in Angle of Repose by Wallace Stegner

I shared my quasi-religious awakening with Stephanie, who, to my relief, was fully into the exposed beam, form-follows-function aesthetic (with the caveat that she was in no position to sign on for timber framing’s DIY ethic any time soon, if ever). That same night, I emailed Shelter Institute, the folks behind the video, and asked them to add me to the waitlist for all 3 of their sold-out timber framing classes in the first half of 2022. I was disappointed to discover the next day that there were over 100 people on each waitlist, all vying for the same unlikely spot to open. Since it was hard to plan anything beyond Stephanie’s graduation in May, I had to put my timber frame dreams on hold. Or so I thought.

There was a time when I couldn’t wait to start drafting these annual reports. And then, 3 years ago, I stopped working. Without income to save, I thought, what did I have to say about saving? Only recently have I begun to appreciate how that sense of the word, what financial planners call “accumulation”, obscures another sense: “preservation”. And maybe I have learned a thing or two about the ebb and flow of preservation.

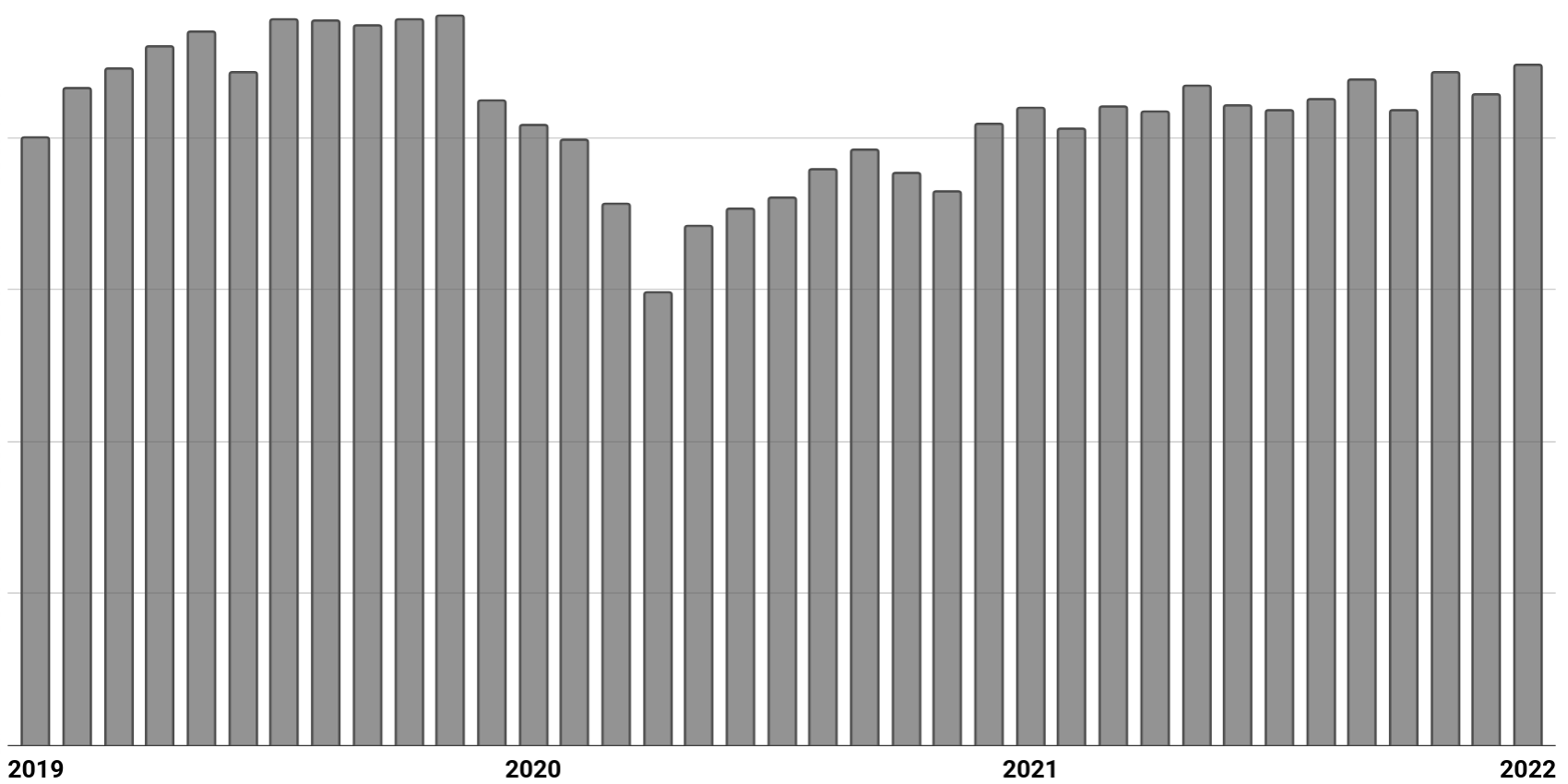

The full extent of our savings (spread across a handful of taxable and tax-advantaged accounts) are still invested in a single S&P 500 index fund. No change there. But without the regular influx of cash from a paycheck, every few months I sell shares from one of our taxable accounts to cover our expenses. Think of it as dollar-cost-averaging on the sell-side. What floors me is how well our taxable accounts have maintained their value over the last 3 years—even in the face of a protracted pandemic.

Monthly value of our taxable accounts from January 1, 2019 to January 1, 2022

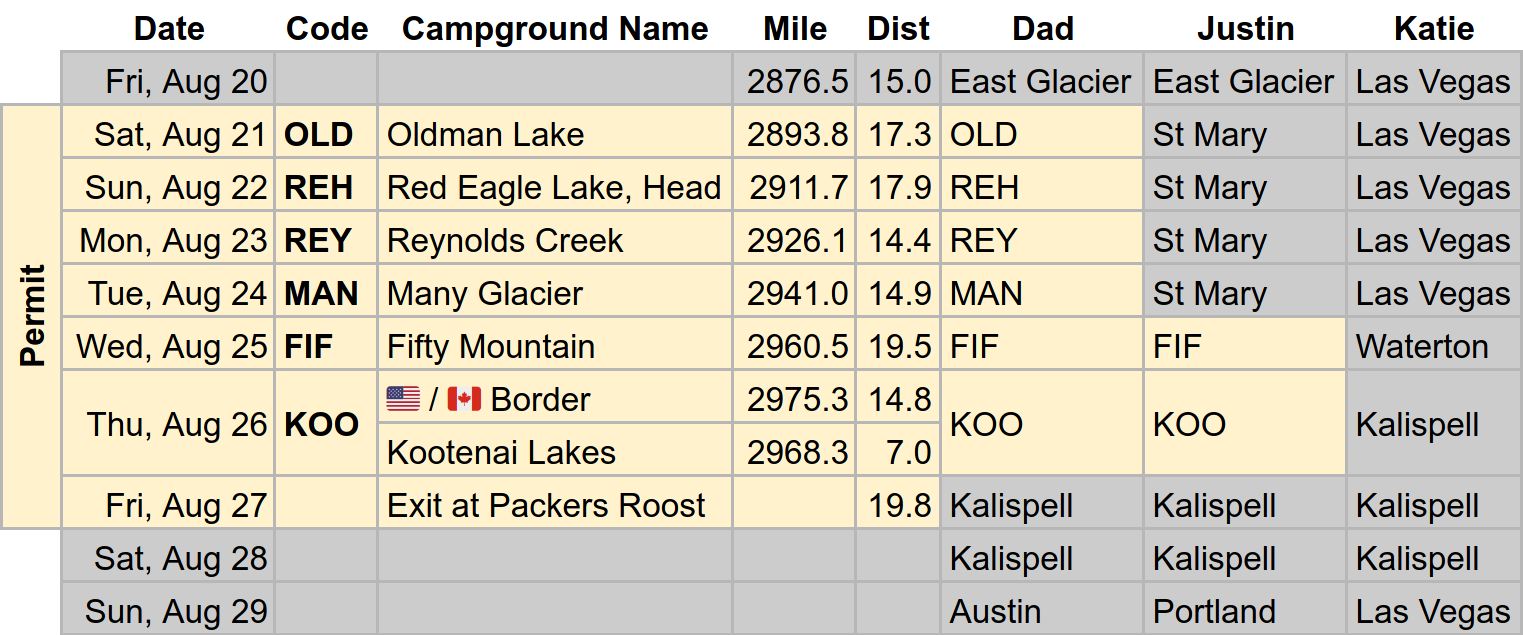

My alarm rang at 3:45 in the morning. I wanted to get in line early to secure a backcountry permit for Dad so he could complete the final 95 miles of the Continental Divide Trail within Glacier National Park. Though my sister had planned to backpack with him to the end, when the border with Canada reopened in early August, Katie opted instead for a mercifully shorter dayhike in Canada’s adjacent Waterton Lakes National Park. Hikers still couldn’t cross the border, but there seemed to be no prohibition against peaceful assembly along the 49th parallel. I was second in line 3 hours before the ranger station opened at 8. Even though I had checked and rechecked the backcountry sites I was going to request, I was still anxious that I might have overlooked some constraint or created a “strange loop” when I accelerated the itinerary after Katie’s plans changed. My nervousness was unfounded. I gave my permit request to the ranger, paid the fee, and walked away moments later, golden ticket in hand.

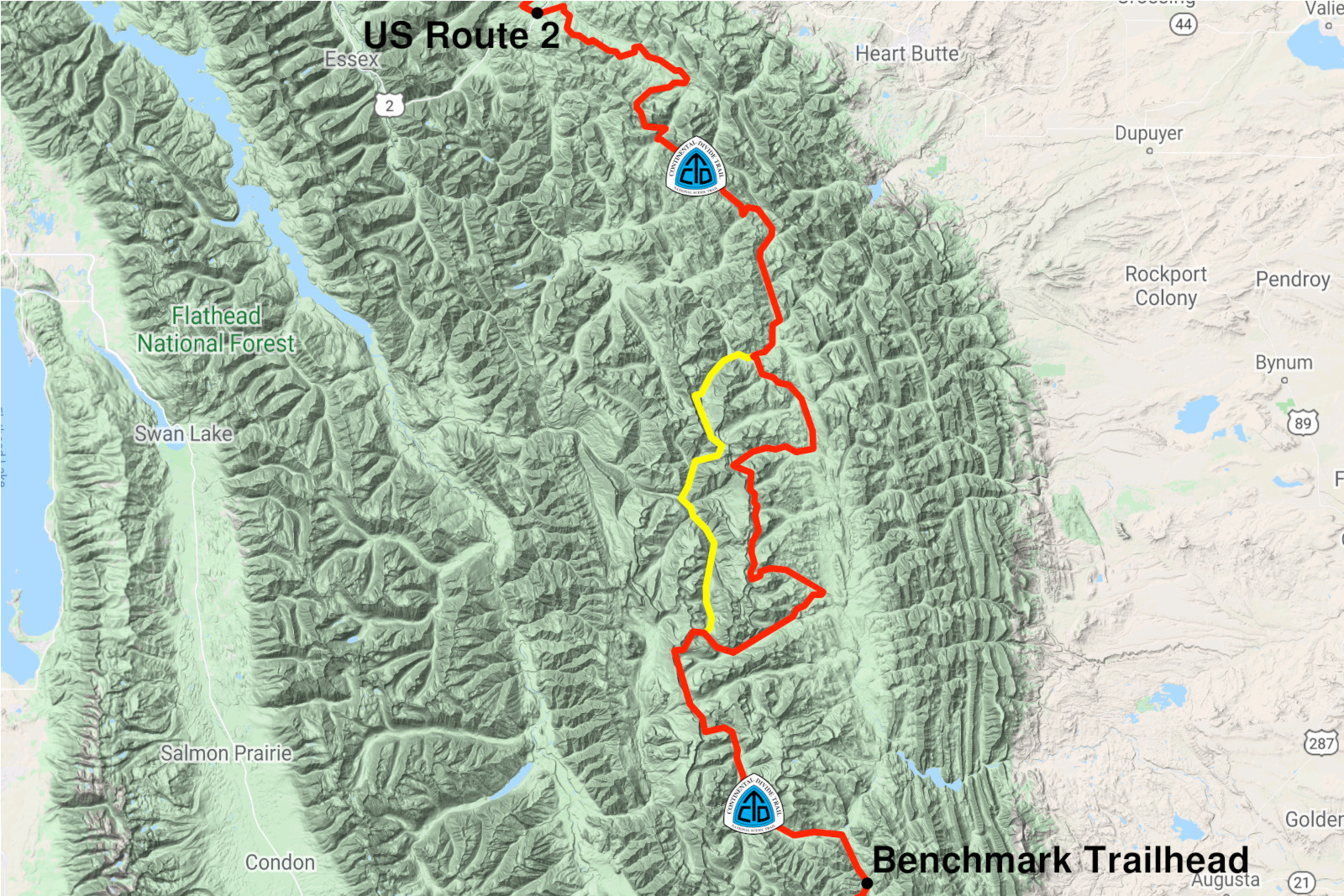

One row, highlighted red, near the bottom of the spreadsheet we use to manage the hike, has been giving us “the evil eye” since the beginning. This row has been threatening Dad with a 118-mile stretch of the CDT in the Bob Marshall Wilderness, between the popular Benchmark Trailhead in the south and US Route 2 in the north—without any intermediate access roads. It so dwarfed every other section that had come before (and will come after) that I was certain there must be a dirt track that crossed the trail somewhere in there. Spoiler alert: there is not.

As directed by the Wilderness Act of 1964, “The Bob”, as it is informally known, is to remain roadless.

The CDT (in red) wending through the Bob Marshall Wilderness